Tags

Facebook IPO, Fraud, Insider Trading, Lawsuit, Main Street, SEC, Securities and Exchange Commission, Stock Market, unwashed public, Wall Street Fraud

It’s nothing new that Wall Street is corrupt and ridden with insider dealings, despite any proclamations or charade enforcement by the Securities and Exchange Commission. To quote Matt Taibbi, “the SEC and Wall Street have been in a wink-wink, nudge-nudge arrangement for years.” And watch this short video discussing the systemic fraud of Wall Street, the SEC, and the judicial system:

What’s also not new is that Main Street continues to pour money into the stock market, only to see it funneled up to the well-connected wealthy investors and banks. As George Carlin always said, “It’s a big club, and you ain’t in it.” Wall Street is just one enormous and slippery greased palm:

Giving well-connected firms an inside track has been one of the ways that big Wall Street firms attract and keep big clients. These clients are powerful profit drivers, and banks tend to give their best customers the best deals.

“These people give them more money in fees and commissions than others,” said Ernest Badway, a former U.S. Securities and Exchange Commission enforcement attorney who is now a white-collar defense lawyer in New York and New Jersey.

“Because of that — they’re part of a great revenue stream — they’re going to try to give every single advantage that they can to those particular people,” he said.

Large institutions and wealthy investors have a symbiotic relationship with Wall Street bankers. “The retail guy is at the end of the queue,” Geisst said. “He can’t do anybody any favors.”

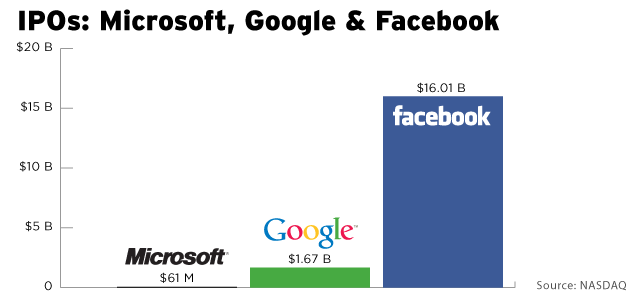

With that in mind, we have the largest tech IPO ever to debut on Wall Street:

Regulators and congressional investigators have begun probes into what went wrong, looking into questions over information distributed ahead of the IPO. Morgan Stanley and other underwriters warned privileged clients that their analysts had grown sour on Facebook’s revenue growth potential. They failed to telegraph the same information to retail clients and the general public. Information affords a crucial trading edge on Wall Street.

“We do not currently directly generate any meaningful revenue from the use of Facebook mobile products, and our ability to do so successfully is unproven. We believe this increased usage of Facebook on mobile devices has contributed to the recent trend of our daily active users (DAUs) increasing more rapidly than the increase in the number of ads delivered. If users increasingly access Facebook mobile products as a substitute for access through personal computers, and if we are unable to successfully implement monetization strategies for our mobile users, or if we incur excessive expenses in this effort, our financial performance and ability to grow revenue would be negatively affected.”

For Facebook to actually be worth $125-$150 billion or more today, it would have to be worth $300-$400 billion in a few years’ time, otherwise it’s not worth buying. Facebook would have to earn $20 billion of profit to justify a $300-$400 billion valuation, 20 times the amount Facebook earned last year. Which means it’s going to have to find new revenue models. And we haven’t seen any evidence of that.

Espen Robak, the president of Pluris Valuation Advisors, has told The Atlantic it doesn’t make any sense. “Nobody knows what Facebook’s revenue and profit model is going to be. If their revenue and profit model stays the same, this valuation doesn’t make any sense. There’s no way they can just squeeze enough plain old ad revenue to justify these numbers. They must change. We don’t know what this is going to look like.”

“The move by GM, one of the largest advertisers in the U.S., puts a spotlight on an issue that many marketers have been raising: whether ads on Facebook help them sell more products. On Friday, Facebook is expected to sell shares in an initial public offering that could put a market value on the company of as much as $104 billion … The move by GM, one of the largest advertisers in the U.S., puts a spotlight on an issue that many marketers have been raising: whether ads on Facebook help them sell more products.

If one were to simply look at polls (half of America thinks that Facebook is just a passing fad while 57 per cent never bother clicking any ads), then you would have to come to the conclusion that the Facebook IPO was just another opportunity for those at the top to siphon off money from gullible ‘investors’. The debacle of the Facebook IPO is a perfect metaphor to sum up America: a nation that has been hollowed out and defrauded by a system that rewards and protects the monied interests of a small elite over the well-being of the rest of the nation.